If one uses a simple random walk with drift estimate over the 2022Q1-2025Q3 period, the answer is yes. However, given the Administration’s internment and removals program, the current projection of population suggests not.

I use a simple error correction model with (log) GDP as the left hand side variable, and GDP and population as an error correction term, estimated over the 1986Q4-2019Q4 ad 2021Q1-2025Q3 period (excluding the pandemic, and with data available to the Troika). I then use the CBO’s reported Census projection of over-16 population to forecast out (the long run elasticity of output with respect to population is 2.1).

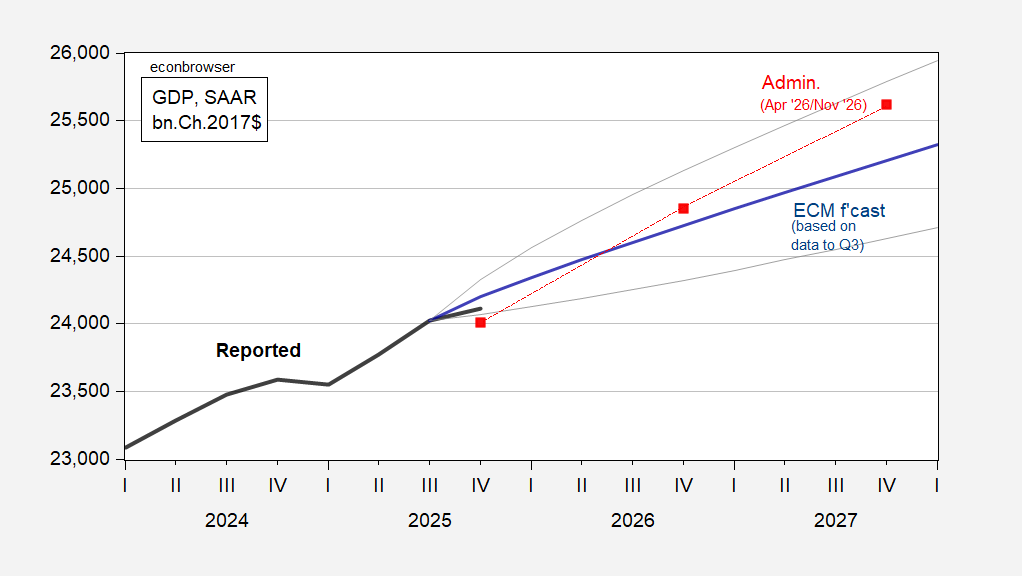

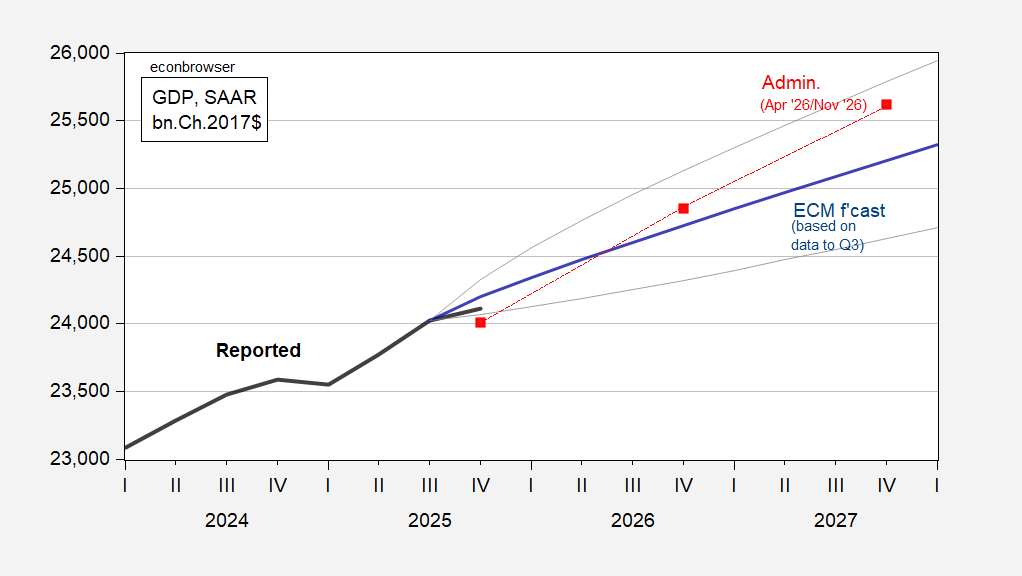

Figure 1: GDP as reported (bold black), Administration FY2027 forecast (red square), ECM forecast using population (blue), +/- standard error band (gray lines), all in bn.Ch.2017$ SAAR. Source: BEA, OMB, author’s calculations.

The Administration’s path is within the +/- one standard error band through 2027Q4, so the forecast is in that sense plausible, based on sampling error. However, the Administration’s path does suggest something interesting about output per capita.

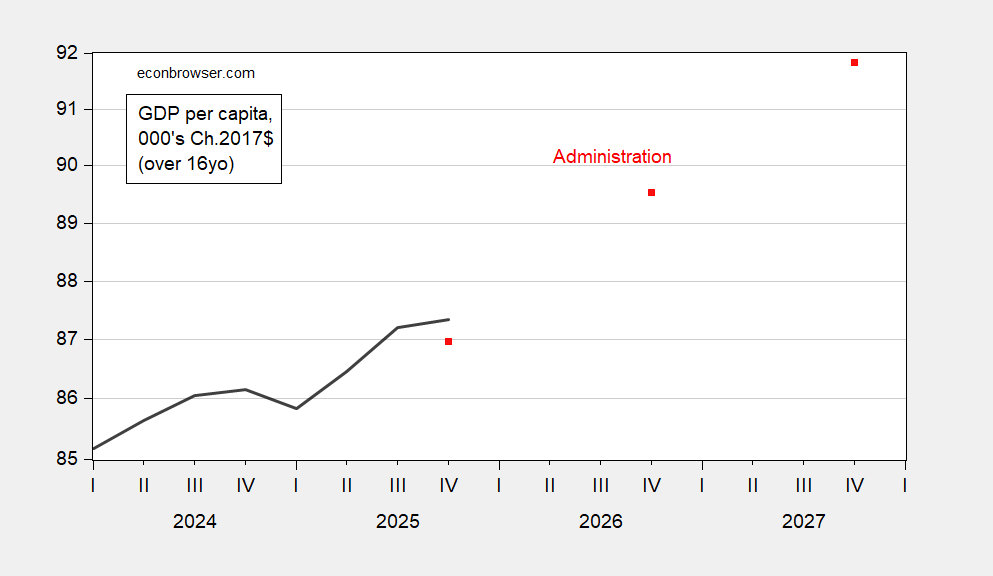

One can work out the implied GDP per capita (counting 16 year old and over):

Figure 2: Output per capita calculated as GDP divided by Census population (over 16yo) (bold black), and implied Administration output per capita (over 16yo) (red square), all in 000’s Ch.2017$, on log scale. Source: BEA, CBO, Administration, and author’s calculations.

The implied growth rate of GDP per capita is 2.9% in 2026, 2.5% in 2027, compared to the current estimate of 1.4% in 2025 (calculations in log differences). Note that these are output per +16yo capita, not output per person-hour in the nonfarm business sector. The only time one sees repeated consecutive instances of such growth is during the dot.com boom, ca 1998…